Tell me why are we, so blind to see

That the ones we hurt, are you and me

-Artis Leon Ivey Jr. (aka Coolio)

That the ones we hurt, are you and me

-Artis Leon Ivey Jr. (aka Coolio)

I'd like to sincerely thank Warren Buffet for so clearly making many of the points I've been trying to make lately in his most-recent submission to Fortune magazine. If anyone hasn't read it yet, it's called 'Why Stocks Beat Gold and Bonds' and you can read it here. Of course, with the King of Bonds himself ringing the closing bell on the bond market just last month, I'm guessing that Warren was aiming at gold more than at bonds with this piece. Bless his heart. Yo Warren B, you're so OG (but your aim ain't quite what it used to be)!

Alrightythen, let's just tear into this juicy carcass and have us a feast!>>>

Warren B: Investing is often described as the process of laying out money now in the expectation of receiving more money in the future. At Berkshire Hathaway (BRKA) we take a more demanding approach, defining investing as the transfer to others of purchasing power now with the reasoned expectation of receiving more purchasing power --after taxes have been paid on nominal gains -- in the future. More succinctly, investing is forgoing consumption now in order to have the ability to consume more at a later date.

Indeed it is! And "saving" (unlike Warren's "investing") is the forgoing of consumption now in order to PRESERVE that purchasing power for a later date. The difference between a saver and an investor is that saving is the passive activity of most people while investing requires a tolerance for the risk of loss and active, specialized knowledge and focus. As I wrote in both Glimpsing the Hereafter and The Studebaker Effect:

"A saver is different from an investor or a trader/speculator. A saver is one who earns his capital doing whatever it is he does, and then aims to preserve that purchasing power until he needs it later. Investors and traders aim to earn more capital by putting their already-earned capital at risk in one way or another. This takes a certain amount of specialization and focus."

Warren B: From our definition there flows an important corollary: The riskiness of an investment is not measured by beta (a Wall Street term encompassing volatility and often used in measuring risk) but rather by the probability -- the reasonedprobability -- of that investment causing its owner a loss of purchasing power over his contemplated holding period. Assets can fluctuate greatly in price and not be risky as long as they are reasonably certain to deliver increased purchasing power over their holding period. And as we will see, a nonfluctuating asset can be laden with risk.

Very good! Yes! Risk is the reasoned probability that you will lose purchasing power over a period of time. Listen up if you happen to be a Berkshire Hathaway investor reading this. I have been spending the last three years working out the reasoned probability that you will lose purchasing power in the near future with your BRKA investment. And over that same holding period, physical gold in your possession is "reasonably certain" to deliver a massive increase in purchasing power. Warren is correct, nonfluctuating assets can be laden with risk while at certain times, the very safest asset will be revalued. Again, as I wrote in both Glimpsing the Hereafter and The Studebaker Effect:

"Today the system is in transition, so you can throw your ideas about these differences out the window. There is no safe medium for simple preservation of purchasing power when the entire system shifts from the old normal to the new normal. When systems implode, the safest place to be pays off big time!"

Warren B: Investment possibilities are both many and varied. There are three major categories, however, and it's important to understand the characteristics of each. So let's survey the field.

Investments that are denominated in a given currency include money-market funds, bonds, mortgages, bank deposits, and other instruments. Most of these currency-based investments are thought of as "safe." In truth they are among the most dangerous of assets. Their beta may be zero, but their risk is huge.

Over the past century these instruments have destroyed the purchasing power of investors in many countries, even as these holders continued to receive timely payments of interest and principal. This ugly result, moreover, will forever recur. Governments determine the ultimate value of money, and systemic forces will sometimes cause them to gravitate to policies that produce inflation. From time to time such policies spin out of control.

Yay! Warren and I agree again! Investments denominated in currency may be nominally safe—if you expect to have a million dollars after a given holding period, you WILL have a million dollars at that future time, but you may only be able to purchase a single roll of toilet paper with that million—but their risk in real terms (purchasing power terms) is HUGE… especially today! It almost seems like Warren has been reading some FOFOA. In any case, here are a few applicable posts that he might have studied:

Moneyness

Deflation or Hyperinflation?

Big Gap in Understanding Weakens Deflationist Argument

Just Another Hyperinflation Post - Part 1

Just Another Hyperinflation Post - Part 2

Just Another Hyperinflation Post - Part 3

Warren B: Even in the U.S., where the wish for a stable currency is strong, the dollar has fallen a staggering 86% in value since 1965, when I took over management of Berkshire. It takes no less than $7 today to buy what $1 did at that time. Consequently, a tax-free institution would have needed 4.3% interest annually from bond investments over that period to simply maintain its purchasing power. Its managers would have been kidding themselves if they thought of any portion of that interest as "income."

Yup! Warren's been around for a long time, alright. And it just goes to show how tough it has been during our entire lifetime for a saver who simply wants to preserve her purchasing power. She has to chase a 4.3% yield every year just to stay even! Crazy, isn't it? What if there was a way to perfectly preserve your purchasing power over any time horizon without chasing a yield? To what percentage of the population do you think that would appeal? Better yet, to what percentage of Warren B's clients do you think that would appeal? Just sayin', what if?

Warren B: For taxpaying investors like you and me, the picture has been far worse. During the same 47-year period, continuous rolling of U.S. Treasury bills produced 5.7% annually. That sounds satisfactory. But if an individual investor paid personal income taxes at a rate averaging 25%, this 5.7% return would have yielded nothing in the way of real income. This investor's visible income tax would have stripped him of 1.4 points of the stated yield, and the invisible inflation tax would have devoured the remaining 4.3 points. It's noteworthy that the implicit inflation "tax" was more than triple the explicit income tax that our investor probably thought of as his main burden. "In God We Trust" may be imprinted on our currency, but the hand that activates our government's printing press has been all too human.

Word. The one-time tax on nominal gains is bad enough, but the vanishing of savers' purchasing power through inflation is the real killer over long time-frames. But why you gotta conflate the issues of real income from an investment and simply protecting one's purchasing power with the least risk, OG? Is this part of your game? Why yes, I dare say I think it is!

Warren B: High interest rates, of course, can compensate purchasers for the inflation risk they face with currency-based investments -- and indeed, rates in the early 1980s did that job nicely. Current rates, however, do not come close to offsetting the purchasing-power risk that investors assume. Right now bonds should come with a warning label.

Holla, G! Maybe the warning label should read – Nothing about this bond, packaging or color should be interpreted to mean safer? How 'bout this one for Berkshire Hathaway – Savers beware, we will try to do more than preserve your purchasing power at the risk of losing your purchasing power, but either way, I was in first, I'll be out first and I always get my cut?

Warren B: Under today's conditions, therefore, I do not like currency-based investments. Even so, Berkshire holds significant amounts of them, primarily of the short-term variety. At Berkshire the need for ample liquidity occupies center stage and will never be slighted, however inadequate rates may be. Accommodating this need, we primarily hold U.S. Treasury bills, the only investment that can be counted on for liquidity under the most chaotic of economic conditions. Our working level for liquidity is $20 billion; $10 billion is our absolute minimum.

I will only note here that, although the link leads to data about bonds, Warren specifically wrote bills which usually means a duration of one, three or six months. Since there is no FDIC protection for cash accounts with $20 billion, T-bills are the guaranteed cash equivalent. This, of course, brings to mind OBA's Time-Currency Theory referencing the subzero-bound $IRX as well asmy conveyance of his theory over the years.

Warren B: Beyond the requirements that liquidity and regulators impose on us, we will purchase currency-related securities only if they offer the possibility of unusual gain -- either because a particular credit is mispriced, as can occur in periodic junk-bond debacles, or because rates rise to a level that offers the possibility of realizing substantial capital gains on high-grade bonds when rates fall. Though we've exploited both opportunities in the past -- and may do so again -- we are now 180 degrees removed from such prospects. Today, a wry comment that Wall Streeter Shelby Cullom Davis made long ago seems apt: "Bonds promoted as offering risk-free returns are now priced to deliver return-free risk."

Ah, now here we start getting a glimpse of Warren's actual game! Notice the word "mispriced" in the above category. This is a key to Warren's strategy, which begins to expose the reasoning behind why he would choose to share this part of his shareholder newsletter with the general public. I realize he's talking about bonds here, but this principle applies to stocks as well (although not necessarily to gold).

Warren likes to buy and sell things that are "mispriced". That is, he knows better than the market the true value of things. And if they are "mispriced" he is, in fact, making money off of the mistakes of others if he turns out to be correct. Bear in mind that I'm not judging him on this issue per se, but simply exposing his game in a way that was most definitely concealed in this latest "newsletter".

Warren, like his lieutenant Charlie M, wants you in the same paper he likes to buy and sell so that he can capitalize on your "mispricing" mistakes. As I wrote inThe Value of Gold, price and value are two different things, and that's Warren B's game:

"Probably the most common misconception is that price and value are the same thing. They are not. They are related but different. Price can be precisely known, but true value can only be estimated or guessed. And because price changes, price is always wrong while true value is always right, even though it is unknown. So price and value are always different. Value is always either higher or lower than price."

Warren will tell you that it's not just about capital gains. Warren LOVES yields, be they high rates of interest or dividends from stocks. But the thing about chasing yields is that the more people chasing, the lower the yield goes, and that's when Warren strikes. That's when things become mispriced. If he was only after yields, he would not want to let the world know what he's doing. But since he's publishing his drive-by on gold in Fortune magazine, I can only assume he's really after the capital gains that will come from the mispricing that will result from millions of people following his "advice".

Warren B: The second major category of investments involves assets that will never produce anything, but that are purchased in the buyer's hope that someone else -- who also knows that the assets will be forever unproductive -- will pay more for them in the future. Tulips, of all things, briefly became a favorite of such buyers in the 17th century.

This type of investment requires an expanding pool of buyers, who, in turn, are enticed because they believe the buying pool will expand still further. Owners are not inspired by what the asset itself can produce -- it will remain lifeless forever -- but rather by the belief that others will desire it even more avidly in the future.

What Warren is referring to here are sometimes called "hard assets". They are durable, physical items that generally hold their value well because people always seem to want them. Like well-preserved classic cars, quality antique furniture or rare baseball cards, hard assets do not generate yields like stocks and bonds. And so Warren is invoking the greater fool theory with regard to hard assets (before even revealing to you the specific one he's targeting) to lay the foundation that YOU are the fool if you think these are a wise way to store your savings.

In fact, if you click on the greater fool link above, you'll find Warren's name right there in the last line. You might also want to click through and read the Keynesian beauty contest principle of stock investing. Warren tells us later just what beautiful stocks look like. They look like Coca-Cola and See's Candy. But if too many people chase those yields, they disappear and even great stocks like that can become mispriced. And that, my friends, is when OG sells!

For example, Berkshire just sold out of its entire position in ExxonMobil after the price surged 17%. Berkshire also sold off Johnson & Johnson and Kraft shares. Fine companies with lots of earnings, so why sell? As for Coca-Cola, that's one of Berkshire's biggest holdings right now! Just sayin'.

Warren B: The major asset in this category is gold, currently a huge favorite of investors who fear almost all other assets, especially paper money (of whose value, as noted, they are right to be fearful). Gold, however, has two significant shortcomings, being neither of much use nor procreative. True, gold has some industrial and decorative utility, but the demand for these purposes is both limited and incapable of soaking up new production. Meanwhile, if you own one ounce of gold for an eternity, you will still own one ounce at its end.

AMEN! Thank you brother. "If you own one ounce of gold for an eternity, you will still own one ounce at its end." Warren's words, not mine. But I'll bet you that I will be milking this quote for a long time to come!

Remember earlier I asked, "What if there was a way to perfectly preserve your purchasing power over any time horizon without chasing a yield? To what percentage of the population do you think that would appeal?" Well, what if physical gold, that singular hard asset that is also held by central banks (precisely BECAUSE it has the fewest industrial uses), was on its way to becoming the singular global reference point for purchasing power, instead of the dollar with everyone chasing a 5.7% annual yield making it harder and harder to catch?

"If you own one ounce of gold for an eternity, you will still own one ounce at its end." In other words, perfectly preserved purchasing power. See? Please read my post Reference Point Revolution for more on this transition that's already underway.

Here is what I am suggesting. That Warren Buffet is the one, regardless of his protestations to the contrary, who is practicing the greater fool theory and the Keynesian beauty contest principle of investing while we, my friends, are the ones who are smartly front running thenetwork effect (aka demand-side economies of scale) and the focal point transformation of the biggest thing in a thousand years.

Warren B: What motivates most gold purchasers is their belief that the ranks of the fearful will grow. During the past decade that belief has proved correct. Beyond that, the rising price has on its own generated additional buying enthusiasm, attracting purchasers who see the rise as validating an investment thesis. As "bandwagon" investors join any party, they create their own truth -- for a while.

On the contrary, homey, it's that the dollar is so overvalued because of the sheer weight brought on by the fact that all dollar "wealth" has a counterparty, and that those counterparties in aggregate can't POSSIBLY perform to expectations in real terms, that a massive adjustment is not only inevitable, but long overdue. EVERYTHING is mispriced right now because the dollar is so massively overvalued at present. And while I can't speak for all gold investors, I'm not buying gold because I think the ranks will grow. In fact, I think the ranks will ABANDON "gold" at the worst time in all of history.

As I wrote in a recent comment, "My scenario… ALLTRADERS dump ALL gold, paper, physical, whatever, in my scenario. It has nothing to do with insiders. It has to do with traders and weak hands." But that's a difficult concept to wrap your head around. If you'd like to try, I wrote about it in my 2010 post, The Shoeshine Boy. The point here is that the true gold thesis is not "the belief that the ranks of the fearful will grow." That is simply Warren Buffet's unfortunate misunderstanding of the gold thesis.

Warren B: Over the past 15 years, both Internet stocks and houses have demonstrated the extraordinary excesses that can be created by combining an initially sensible thesis with well-publicized rising prices. In these bubbles, an army of originally skeptical investors succumbed to the "proof" delivered by the market, and the pool of buyers -- for a time -- expanded sufficiently to keep the bandwagon rolling. But bubbles blown large enough inevitably pop. And then the old proverb is confirmed once again: "What the wise man does in the beginning, the fool does in the end."

It is so incredibly striking to me that "the best of the best," the Oracle of Omaha himself, is still reciting these same tired old arguments. It simply defies logic that Warren Buffet is comparing gold to the housing and dot-com bubbles to save you out of the goodness of his heart. If he doesn't want you engaging in a "bubble", it's only because he wasn't there first. In fact, there are plenty of gold bugs who actually THINK gold will eventually be a bubble, and that's precisely why they're in it. But not me.

More than two years ago I debunked the ridiculous and shallow comparison of gold to past bubbles in Gold: The Ultimate Un-Bubble:

"And since gold production cannot be ramped up to meet demand like it can in bubblicious items, there is no reason for gold to fall back. Gold mining does not debase gold in the same way that dollars, tulips, homes, Dot Com IPO's or government bonds are debased through production. Mine production is taken from known reserves that are already valued, owned and traded, and all gold on the planet Earth is a fixed amount, the same fixed amount it was a million years ago. All we do is move it around, like poker chips on a table, to those savers that value it the most.

Furthermore, the price of gold is completely arbitrary. This means that gold can go as high as the people of Earth want to take it without EVER exceeding objective valuations by common metrics like earnings, interest or the sum value of its component elements. Gold IS the element. It cannot be broken down further, except perhaps by the LHC.

One of the most common criticisms of gold's use as an investment is that it cannot be valued the way stocks, bonds and real estate can. They are all commonly valued by their yields, and gold has no yield, therefore it cannot be fairly valued, or so the argument goes. But if we invert this argument then gold can never be OVERvalued either, whilst those other things can, and are... in a bubble!

The price of gold is arbitrary, ergo, there is no such thing as a gold bubble."

Of course that is not the whole story, it's only a teaser from the post. But the point is that if Warren Buffet is truly avoiding gold because he thinks it's a bubble like Pets.com or Miami condos, you should really question EVERYTHING that comes out of his mouth. Now I will admit that PAPER gold is a bubble, but physical gold? Never!

Warren B: Today the world's gold stock is about 170,000 metric tons. If all of this gold were melded together, it would form a cube of about 68 feet per side. (Picture it fitting comfortably within a baseball infield.) At $1,750 per ounce -- gold's price as I write this -- its value would be about $9.6 trillion. Call this cube pile A.

Let's now create a pile B costing an equal amount. For that, we could buy all U.S. cropland (400 million acres with output of about $200 billion annually), plus 16 Exxon Mobils (the world's most profitable company, one earning more than $40 billion annually). After these purchases, we would have about $1 trillion left over for walking-around money (no sense feeling strapped after this buying binge). Can you imagine an investor with $9.6 trillion selecting pile A over pile B?

No, and neither can I imagine a saver with a regular job, a life to live, an aversion to risk and a desire to merely preserve his purchasing power wanting to own a bunch of oil and farming companies. Besides, if Exxon Mobil is so profitable, why did Warren just sell his entire stake in it? Could it be that even profitable companies become mispriced (overvalued) when everyone is chasing a yield?

Okay Warren, can I imagine an investor with $9.6 trillion buying all the gold in the world? Of course not. No choice could be more stupid if such a person could exist. As I have written many times, gold would be completely worthless if one person (or even just a few people) owned it all. Gold's greatest value comes from its widest distribution amongst savers, and the greater the value, the more efficiently gold performs its primary function. It is a virtuous and self-sustaining feedback loop. From Relativity: What is Physical Gold REALLY Worth?:

"One of the unique characteristics of gold that sets it apart from commodities is that its primary use - store of value - has no weight or mass requirements. In commodities, where industry is the primary user, weight is critical.

[…]

One ounce [of gold] could do just as good of a job as 100 ounces. In fact, one ounce would do a BETTER job than 100 ounces! The less gold it takes to store your value, the better it does its job. This particular “gold dynamic” sets it apart from all commodities.

One ounce would store your value more efficiently and stably than 100 ounces because A) your storage and security costs would be lower (efficiency), and B) if one ounce is worth $100,000 then that infers gold is being valued by many more people relative to when it was $1,000 per ounce. This wider distribution brings with it a more stable base of valuation and less relative volatility in price (stability).

Comparing this “gold dynamic” to any industrial or food commodity we can see a stark difference. What commodity could perform its job BETTER at a price 100x higher than today? Can you name one?"

And from a comment in 2009:

"Gold would not be valuable if one person owned all of it. It is most valuable in its widest distribution possible, the wealth reserve, which requires a much higher valuation than it has right now. A higher valuation denominated in hard assets, not just fiat currencies!"

And another comment from 2010:

"Just look at the BIS' own gold actions. Their owned gold hoard has shrunk from 194 tonnes to 120 tonnes over the last 6 years, as has the entire Eurosystem's hoard over the last decade (from 12,576 tonnes down to 10,833 tonnes). Most gold movements in Europe have either been lateral reshuffling or dishoarding and encouraging citizens and other entities to start hoarding physical gold themselves.

I have written this before... if you were King of the World with 35,000 tonnes of gold in a world of 160,000 tonnes, you would gladly - happily - reduce your "stash" to 10,000 tonnes if that reduction came with a 50x revaluation. Trying to get ALL the gold into your hoard is a fool's strategy."

Like I said, Warren, buying all the gold in the world would be about the dumbest thing such an investorcould possibly do, kinda like a doctor owning an oil company and calling it savings.

Warren B: Beyond the staggering valuation given the existing stock of gold, current prices make today's annual production of gold command about $160 billion. Buyers -- whether jewelry and industrial users, frightened individuals, or speculators -- must continually absorb this additional supply to merely maintain an equilibrium at present prices.

Hahaha! B's worried about who's gonna buy up the annual physical gold production? How about who's gonna keep buying the annual paper production bearing dubious counterparties in the upper left-hand corner? I think it's Warren B who is worried about who's gonna keep buying the stuff he's into.

With well over $100T in cash, cash equivalents, debt and equity investments posing as savings for the risk-averse, I think it's more than safe to say that ANOTHER had it exactly right when he said that the paltry $160 billion flow of gold is (and has been for a long time) cornered. Heck, nearly a third of that is going to India alone, and they aren't even one of the surplus nations like Saudi Arabia, Germany or China!

Warren B: A century from now the 400 million acres of farmland will have produced staggering amounts of corn, wheat, cotton, and other crops -- and will continue to produce that valuable bounty, whatever the currency may be. Exxon Mobil (XOM) will probably have delivered trillions of dollars in dividends to its owners and will also hold assets worth many more trillions (and, remember, you get 16 Exxons). The 170,000 tons of gold will be unchanged in size and still incapable of producing anything. You can fondle the cube, but it will not respond.

Fondle the cube? Alrightythen, no more Mr. Niceguy here either. Once again, Warren, why did you sell Exxon if it's so great and saving money is all about dividends and earnings rather than taking (OPM) money from the greater fool? What a hypocrite! Is it also possible that companies can be mismanaged, like, say, BAC?

Here are a few other "good companies" that Berkshire dumped since it (BRKA) took a 50% nose-dive in 2008 (actually late 2007 to early 2009): Nike, Comcast, Lowes, Home Depot. And in case you are still under the illusion that OG is all about solid, benevolent analysis rather than political monies for OG's pocket, his company is still the largest shareholder in Wells Fargo (NYSE: WFC)and "he has practically bought at any chance he gets." Nothing against Wells Fargo (I have an account there) but this, combined with his drive-by assault on gold (the hard asset preferred by those who actually produce stuff) should settle any debate about whether or not he carries a bias in his baggage.

Warren B: Admittedly, when people a century from now are fearful, it's likely many will still rush to gold. I'm confident, however, that the $9.6 trillion current valuation of pile A will compound over the century at a rate far inferior to that achieved by pile B.

"Pile A" does not compound. It simply remains. Remember? "If you own one ounce of gold for an eternity, you will still own one ounce at its end." That said, there's no guarantee that pile B will be worth more than pile A in 100 years. A lot can happen in 100 years, wars, hyperinflations, companies go bankrupt… If you were to be put into a deep sleep coma-like state for a century, and you had trillions in wealth, which pile would you pick to shuttle your wealth through 100 years?

Warren B: Our first two categories enjoy maximum popularity at peaks of fear: Terror over economic collapse drives individuals to currency-based assets, most particularly U.S. obligations, and fear of currency collapse fosters movement to sterile assets such as gold. We heard "cash is king" in late 2008, just when cash should have been deployed rather than held. Similarly, we heard "cash is trash" in the early 1980s just when fixed-dollar investments were at their most attractive level in memory. On those occasions, investors who required a supportive crowd paid dearly for that comfort.

And finally, here's the argument that only Helen Keller could believe, that today's contrarian is staying as far away from gold as possible. Especially that physical gold. Look at the lines to buy gold at the dealers. They wrap around the block. You can't find a place to eat these days without having some dolt at the next table talking about gold. Heck, even the shoeshine boy can tell you what coins are best and where to buy. It's obviously a bubble. Yeah, right.

Warren B: My own preference -- and you knew this was coming -- is our third category: investment in productive assets, whether businesses, farms, or real estate. Ideally, these assets should have the ability in inflationary times to deliver output that will retain its purchasing-power value while requiring a minimum of new capital investment. Farms, real estate, and many businesses such as Coca-Cola (KO), IBM (IBM), and our own See's Candy meet that double-barreled test. Certain other companies -- think of our regulated utilities, for example -- fail it because inflation places heavy capital requirements on them. To earn more, their owners must invest more. Even so, these investments will remain superior to nonproductive or currency-based assets.

By superior, he means that he views investing as superior to saving. He is, after all, an extraordinary investor. But most of his audience is, in fact, made up of savers. As far as savings go, for the near future (i.e., the transition period) gold will be far superior to Warren's investments as the transition brings REAL gains of tremendous value to those who hold the goods. And in the distant future, physical gold will be a far superior savings medium as it will be the very benchmark of purchasing power everywhere. In that future, owning companies will potentially bring you real returns whereas gold will not. But it will also carry risks and responsibilities. And if you carry gold from here into that future, you will be one of the fortunate few faced with that choice.

Warren B: Whether the currency a century from now is based on gold, seashells, shark teeth, or a piece of paper (as today), people will be willing to exchange a couple of minutes of their daily labor for a Coca-Cola or some See's peanut brittle. In the future the U.S. population will move more goods, consume more food, and require more living space than it does now. People will forever exchange what they produce for what others produce.

Absolutely true! In fact, this is the Debtors & Savers Zone he is describing. The part of the pyramidsoccupied by everyone!

What's missing in his description is what the savers will trade amongst themselves to perfectly preserve their purchasing power during periods of deferred consumption. Sure, someone will own all those companies OG loves so much. And like I said, if you carry some of that physical gold from here into that future, it might just be you!

Warren B: Our country's businesses will continue to efficiently deliver goods and services wanted by our citizens. Metaphorically, these commercial "cows" will live for centuries and give ever greater quantities of "milk" to boot. Their value will be determined not by the medium of exchange but rather by their capacity to deliver milk. Proceeds from the sale of the milk will compound for the owners of the cows, just as they did during the 20th century when the Dow increased from 66 to 11,497 (and paid loads of dividends as well).

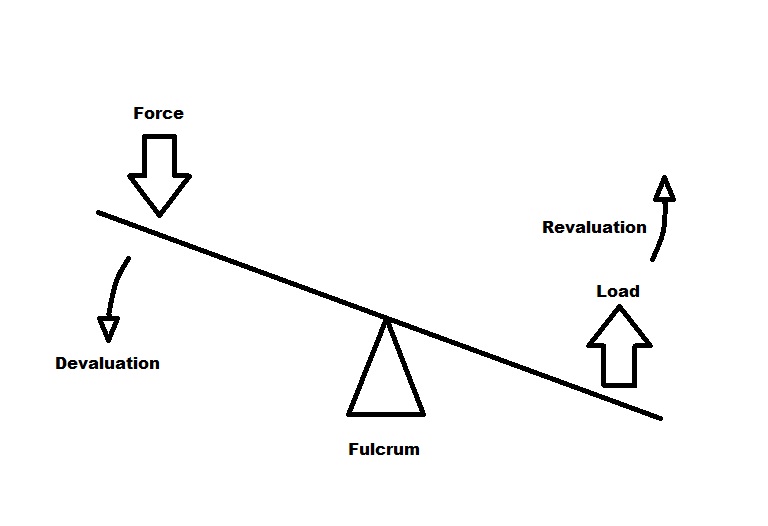

Of course they will, Warren! No one at this blog is predicting the collapse of modern society. The gold thesis discussed here is about that which is mispriced (overvalued or undervalued) coming back in line with reality. The dollar is overvalued and physical gold is undervalued. I described it as a seesaw in The Studebaker Effect:

"Devaluations play out like a seesaw. There is a force (the crisis devaluation), a fulcrum (what is being devalued against), and a load (the beneficiary or the winner)."

That fulcrum is the physical plane of goods and services in aggregate. Everything is mispriced today, some things more than others. But if we look at how Warren's favorite investments, company stocks, carried through past devaluations, we find that while they obviously do much better than currency or currency-based investments like bonds, they don't do quite as well as hard assets and they don't even preserve purchasing power. Perhaps it's because an overvalued currency also tends to overvalue its economy.

Here's a bit from my post Greece is the Word on how Warren's equities might fare during the currency devaluation he expects:

"But what about the stock market? Someone emailed me saying,

"During a currency crisis in the western world, we may see a very powerful stock market rally as equities are a form of real asset. Better to own a piece of Procter and Gamble than a unit of currency that can devalue quickly. Look to the Argentina general equity market MERVAL index during the peso crisis. It shot up – although not as much as the 3:1 currency devaluation."

The writer answered his own point. The stock market shot up LESS than the currency devalued. So while the stock market in Argentina performed MUCH better than debt fixed to the value of the currency, it only chased - and lagged - actual inflation. (Actually, short term hyperinflation.)This is partly because the economy is usually in shambles at the time of a currency devaluation. So while you would expect real things like real companies to compensate for a falling currency, you must also weigh in any previous bubbling that might deflate and any economic factors that might reduce company profits.

But Argentina is still a good example for us to look at. In January of 2002 the currency devalued 3:1. At the same time the stock market rose in response to the devaluation and then stayed up (because the currency stayed down). But what is interesting about Argentina is that just prior to the devaluation, in December of 2001, inflation dipped into negative territory (deflation?) and the stock market dipped as well. Then they almost immediately exploded out of this head-fake in an unexpected devaluation. See the charts. The first is the MERVAL and the second is CPI:

Hmm... look familiar?

Bottom line: The stock market, because it represents equity not debt, will fare much better than the rest of the paper world. But the stock market does suffer from dilution, manipulation and bubbles. Expect the stock market to languish in economic chaos as it chases real inflation only to fall a little short.

But gold is different. The system desperately needs a counterweight, and gold is it. The counter is already in place, only the weight is yet to come. And once we have seen the reset in gold as it performs its phase transition from commodity to wealth reserve, it will then chase (hyper)inflation along with the rest of the "non-dollar" world, only it will be the ONE AND ONLY THING that will be immune to the economic mess that will still need to be worked out."

So what we can do is to place Warren's favs just to the left of the fulcrum on the seesaw. They won't devalue much in real terms, but they also won't fare even as well as boring old hard assets like antique furniture (I'm sure he'll just love this one):

Warren B: Berkshire's goal will be to increase its ownership of first-class businesses. Our first choice will be to own them in their entirety -- but we will also be owners by way of holding sizable amounts of marketable stocks. I believe that over any extended period of time this category of investing will prove to be the runaway winner among the three we've examined. More important, it will be by far the safest.

And thus ends Warren B's drive-by assault on gold. What do you think? Did he hit his target?

So where is Warren coming from?

Try to imagine a bizarro world where we simultaneously encourage everyone to consume as much as possible through debt (because, ldo, consumption is the engine of the American economy) and also to save that same debt through ERISA and 401(k)s. What you end up with is a whole society of people deferring consumption (saving) on the one hand, and pulling into the present that very same future consumption they saved on the other. You end up with underwater homeowners with negative net-worths and hundreds of thousands sitting in their 401(k) or IRA.

With everyone chasing a yield, be it through interest rates on currency investments or dividends from equities, you eventually drive all those yields to zero. Luckily for the Warren Buffets of the world, most of that "savings" knows no better than to float around in Warren's world, where Warren not only gets his management cut, but he can also make amazing capital gains as those "savings" slosh around mispricing one thing after another.

Now think about that person, let's call him Bob, with $201K in debt and also a $200K pension or IRA through work. In essence, he could be almost debt-free were it not for his "savings". But then if that were the case, Warren wouldn't have that $200K sloshing around in Warren's world. This is, of course, only a mental exercise in how inane (or should I say insane?) the Western financial system really is.

Which camp do you think Bob is in? The Debtors or the Savers? And what would be the state of Warren's company valuations were it not for all this additional "savings" sloshing around? How about the yields available for real savers? Perhaps there would be some yields to be found were it not for Bob and his "savings"?

The point is that companies are not de facto good investments just because they make things. They can become overvalued when chased by too much money and that's when Warren sells. Warren talks a good talk about compounding dividends, but what he's really after is your money. Either you're with him (investing in BRKA) and he takes his cut while using your financial weight as his own, or you're against him out there on your own. And then he's looking for areas where you've mispriced something so that he can buy it from you or sell it to you.

I can tell you which camp OG is in. He's in the easy money camp (the debtors)! He's in debt to easy money:

Warren Buffett is on Squawkbox right now defending the bailout, which he wrote an op-ed about in today's New York Times.

Then he dropped this line, which sounds like an exaggeration: "If the government hadn't acted, I would be eating Thanksgiving dinner at McDonald's."

(Business Insider)

Perhaps he wasn't exaggerating:

A good chunk of his fortune is dependent on taxpayer largess. Were it not for government bailouts, for which Buffett lobbied hard, many of his company’s stock holdings would have been wiped out.

Berkshire Hathaway, in which Buffett owns 27 percent, according to a recent proxy filing, has more than $26 billion invested in eight financial companies that have received bailout money…

…It takes remarkable chutzpah to lobby for bailouts, make trades seeking to profit from them, and then complain that those doing so put you at a disadvantage.

Elsewhere in his letter he laments “atrocious sales practices” in the financial industry, holding up Berkshire subsidiary Clayton Homes as a model of lending rectitude.

Conveniently, he neglects to mention Wells Fargo’s toxic book of home equity loans, American Express’ exploding charge-offs, GE Capital’s awful balance sheet, Bank of America’s disastrous acquisitions of Countrywide and Merrill Lynch, and Goldman Sachs’ reckless trading practices.

And what of Moody’s, the credit-rating agency that enabled lending excesses Buffett criticizes, and in which he’s held a major stake for years? Recently Berkshire cut its stake to 16 percent from 20 percent. Publicly, however, the Oracle of Omaha has been silent.

(Reuters)

So maybe you are starting to see why Freegold is not such a welcome development for an OG like Warren B. But don't worry too much about Warren. He'll still be a multi-billionaire come Freegold. And if you follow him, at least you won't be broke (see the seesaw above). I suppose there might even be something altruistic about leaving the Freegold revaluation windfall for others. But that's not Warren's motivation.

Warren's power comes from keeping as much of other people's savings as possible in the stock market where he plays. It doesn't matter if it comes in through his company or on its own, just that it's in there. And that's why he wrote this piece trashing gold. Because when you buy a tube of gold coins and put it in your sock drawer, it's out of OG's reach.

Sincerely,

FOFOA

Power in the money, money in the power

Minute after minute, hour after hour

Everybody's runnin, but half of them ain't lookin

At what's goin on in the kitchen, but I dont know what's cookin

They say I gotta learn, but nobody's here to teach me,

If they can't understand it, how can they reach me?

I guess they can't; I guess they won't

I guess they front; that's why I know my life is outta luck, fool!

We've been spending most our lives

Living in a Gangster's Paradise

Source