The German Federal Audit Office has criticized lax Bundesbank controls of and management of Germany's 3,396.3 tons in gold reserves. It is believed that some 60% of Germany's gold is stored outside of Germany and much of it in the Federal Reserve Bank of New York, to facilitate payment and trade, according to German newspaper Bild. A Parliamentary Budget Committee will assess how the bank manages the inventory of bullion totaling 42% of Germany's money held as savings in reserve.

Other central banks will follow Hugo Chavez's "mission accomplished" (Detail Here), and now Germany's footsteps in bringing home - repatriating - their gold, retaining direct possession of and therefore true ownership, not multiple paper promises of ownership (re-hypothecated).

Good timing for this type of news, as paper gold shorting has escalated as of recent and can absorb the bids which this news prompted, preventing a paper price spike much higher than the goal of maintaining order allows.

Good timing for this type of news, as paper gold shorting has escalated as of recent and can absorb the bids which this news prompted, preventing a paper price spike much higher than the goal of maintaining order allows.

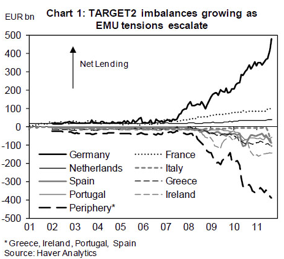

These moves are important in order to be better prepared for systemic crisis. Clearly this concern is developing, as moves in gold custody become more frequent. If the eurozone were to collapse under the 37x leveraged €3 trillion balance sheet chock full of non-performing "assets" the Bundesbank's losses would total near €500 billion, more than 150% of GDP. Chart above current to January 2012.

Should the ECB and the Euro collapse, the gold would be needed to support the Deutschmark currency. This argument alone does not mean the gold needs to be repatriated as Germany is backing the Euro currency system today with their gold being held abroad. The real problem is that the gold held at the Fed could simply be confiscated in order to satisfy dollar swap agreements with the ECB, should they be unable to repay due to an epic collapse. This type of event, leading to intensification of the currency wars, brings the 'nuclear option' of a drastic upward revision of the price of gold into view. Confidence in re-hypothecated or multiple concurrent gold loans is collapsing, meanwhile the price of loaning gold is at a high.

This type of event, leading to intensification of the currency wars, brings the 'nuclear option' of a drastic upward revision of the price of gold into view. Confidence in re-hypothecated or multiple concurrent gold loans is collapsing, meanwhile the price of loaning gold is at a high.

This act of repatriating physical within the anglo-system, is in itself an acknowledgement of a return to a quasi gold standard. Nothing more than confidence backs the inverted currency pyramid, and this is confidence lost by those who administer the system.